SBI card IPO – Date, review, listing date

Page Contents

SBI card IPO – Date, review, listing date

SBI card IPO; with this IPO Indian investors will have a chance to invest in credit card companies as there is no other listed company in stock market which only focuses on Credit card business.

SBI card IPO Date and details

| SBI Cards IPO Details | |

| Issue Open | Mar 2, 2020 – Mar 5, 2020 |

| Issue Type | Book Built Issue IPO |

| Issue Size | 10286.20 Crores |

| Fresh Issue | TBA |

| Offer for Sale | TBA |

| Face Value | ₹10 Per Equity Share |

| Issue Price | Rs 750-755 Per share |

| Market Lot | 19 |

| Min Order Quantity | 19 |

| Bid/Offer Opens On | Mar 2, 2020 |

| Bid/Offer Closes On | Mar 5, 2020 |

| Finalisation of Basis of Allotment | Mar 11, 2020 |

| Initiation of Refunds | Mar 12, 2020 |

| Credit of Shares to Demat Acct | Mar 13, 2020 |

| IPO Shares Listing Date | Mar 16, 2020 |

SBI Card IPO details:-

The equity share capital of the company as on the date of filing the DRHP is 93.23 Cr shares of Rs 10 each. 74% of this or 68.99 Cr shares is held by SBI(promoter) and 26% or 24.24 Cr shares by CA Rover Holdings, an affiliate of the Carlyle Group.

Carlyle Group entered the business in 2017 by buying out the stake of GE Capital, who had been associated with the company for over two decades. GE Capital’s stake sale was bought by both SBI and CA Rover. CA Rover paid Rs 2,000 Cr for its 26% stake, valuing the company at Rs 7,700 Cr at that point.

Below is how the shareholding has changed over the last two years

The company will sell 14% of its equity in the IPO. The details of this issue are

- A fresh issue of shares to the tune of Rs 500 Crs

- Offer for sale (OFS) of 13.05 Cr shares which includes

- Employee reservation portion of 18.64 Lakh shares and

- SBI shareholders reservation portion of upto 1.30 Cr shares. Investors can apply in this category if they hold SBI shares on the day when the DRHP has been filed with SEBI

SBI will sell 3.72 Cr shares or 4% and CA Rover 9.32 Cr shares or 10%. The company hasn’t given any details about the price at which it is going to offer its shares. It is however estimated that the 14% stake sale will fetch the company anywhere between Rs 8,000 – 9,500 Cr. This pegs the value of the company in the range of Rs 58,000 – 68,000 Cr. At these valuations CA Rovers stake will be valued at about 15,000 – 17,700 Cr. It will make 7-9X on its investments made a couple of years back.

The fresh issue of shares is 500 Cr, these will be used to strengthen the company’s capital base and ensure its compliance with RBI directives. SBI Cards is registered as NBFC – ND – SI (non-banking finance company – systemically important non-deposit taking company).

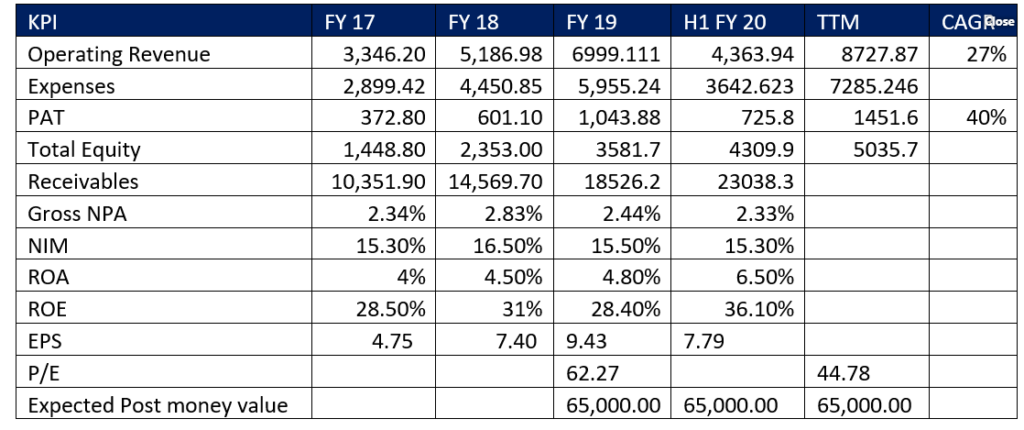

SBI card IPO Valuation

- It is expected that the Post IPO ( At issue price) valuation of SBI cards will be 65000 Crore.

- In 2017 GE capital exited from credit card business and sold an entire 40% stake in SBI cards to SBI and CA Rover Holdings. CA Rover Holdings bought 26% stake for INR 2000 Crore valuing entire company worth Rs. ~7000 Crore.

- The expected post-money value of the company is about INR 65000 Crore. I.e. CA Rover holding may get INR 6500 crore for 10% stake valuing their entire stake worth INR 16900 Crore. Its massive 8.5x return in just 3 years.

- With PAT of INR 1043 crore (FY 19) and valuation of about INR 65000, the Company is available at an earnings multiple of 62.27 times. This parameter company looks a bit overvalued though there is no peer listed player in the Indian market. However, revenue CAGR of the past 4 years is 27% and PAT CAGR is 40%.

- This kind of growth along with an average 4 years ROE of 31%, NIM of 15.5% and gross NPA of just 2.5% justify the value of the company.

Credit Card Industry overview in India

Credit cards fall into the unsecured loan category, the other loans which fall into this segment are personal loans and consumer durable loans. The unsecured loan market at the end of FY19 was estimated to be Rs 5 trillion. 73% of this comprises of personal loans, 22% credit cards and 5% consumer durable loans.

Unsecured loans have been the fastest-growing category in retail credit, registering a 28% CAGR in the FY14-19 period.

Delinquency in personal loans is in the range of 0.5-0.7%, credit cards 1.5-1.8% and consumer durable loans 1.5-2%.

Some of the salient features of the credit card market in India are

- Credit card spends in FY19 amounted to Rs 6 trillion, registering a 32% CAGR over the last 5 years. Spends are expected to 2.5X (15 Trillion) by 2024

- Number of credit cards issued – 47 million at the end of FY19. Numbers/Volumes have grown by 20% CAGR over the last 5 years. Cards outstanding at the end of October 2019 – 53.4 million

- Average annual spends per credit card – Rs 1,44,000, registering a growth of 12% CAGR over the last 5 years

- Sales of credit cards happen mainly through distribution channels like Banca (selling at existing bank customers) and open market (malls, petrol pumps, airports, retail stores etc.)

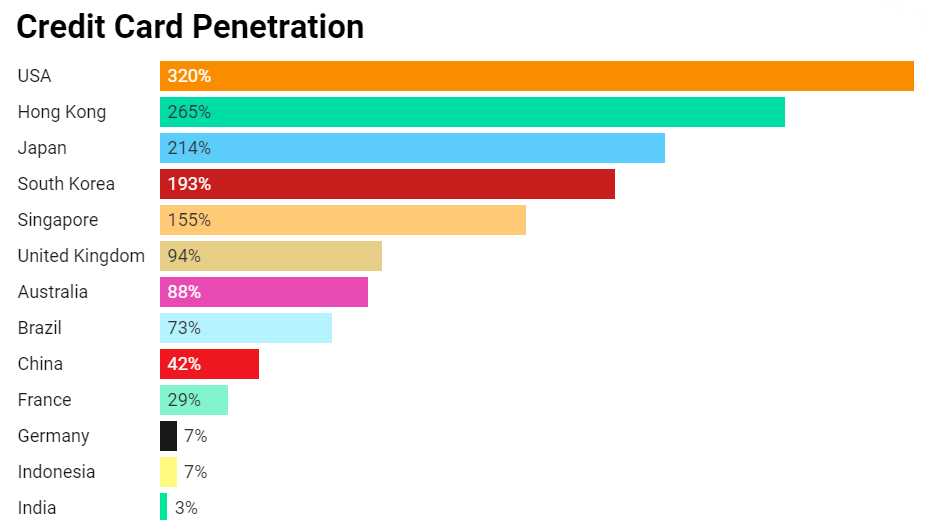

- Credit card penetration (average number of cards per 100 people) in India is low – 3% in FY19 as compared to other countries. On the other hand debit card penetration in the country is at 65%

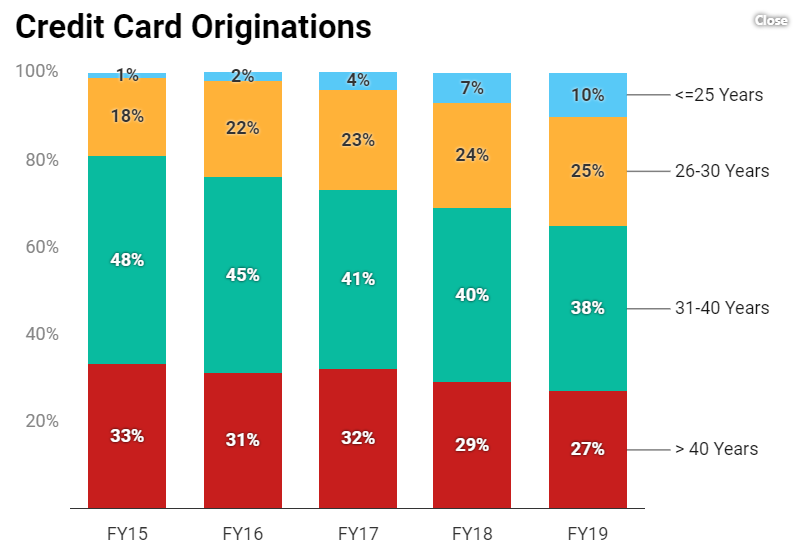

- Credit card originations among millennials (people below 30 years of age) has increased over the last 4 years from 19% to 35%, the share of customers below the age of 25 has increased 10X in the same period

- Demonetization, digitalization, cashless society, development in the e-commerce space and improved payment infrastructure (POS terminals and payment gateways) have lead to the faster growth of credit cards over the last few years

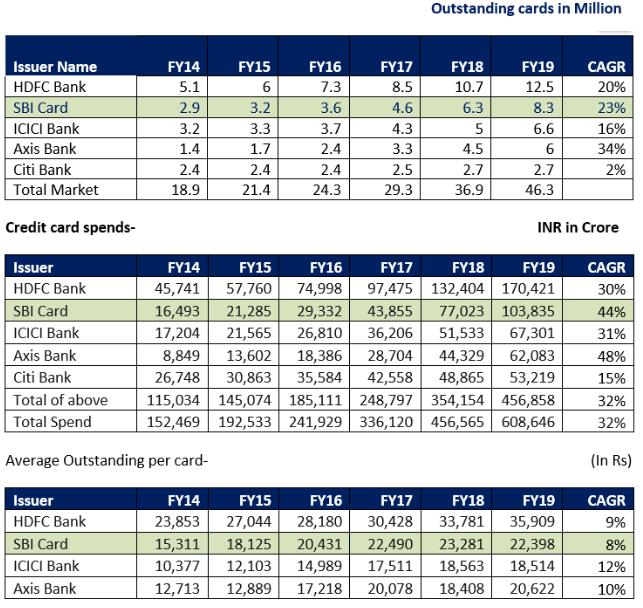

- HDFC is the market leader in No of card outstanding as well as average spends and outstanding while SBI cards is second largest player with market share of 18%

- 5 Year CAGR of no of cards is 23% while credit cards spend is 44%

- Asset quality is stable with gross NPA of 2.5% as on March 19

- SBI cards has co- branded cards with IRCTC,BPCL, OLA, Air India and Apollo Hospital

- Receivables as on 30st Sep 2019 is 23038 Crore

- Average yield is about 21% and NIM is about 15%

- ROA is 4 to 4.8%

Growth Factors –

- The E-commerce industry in India is growing at a pace of 32% CAGR in the last 5 years and is expected to grow at 25% CAGR over the next 5 years.

- E-com industry size was INR 713 bn. In FY 14 in FY 19, it reaches to INR 3000+ bn and expected to cross INR 9000 bn by FY 24. Most of the E com companies started accepting Cards payment in COD (cash on delivery) Cards spends likely to be increased.

- The median age of India is 28 years new credit card origination has shown the highest growth in the age group of 20-30 years.

- Organized retail penetration (including E-com) is just 11% and is expected to be about 15% by FY 24

- With deeper penetration of payment networks of PayTM and PhonePay and credit card spends are increasing.

- Promoter advantage, about 70% of the customers sourcing done by SBI.

Source – equialpharesearch

Earning source for SBI Card

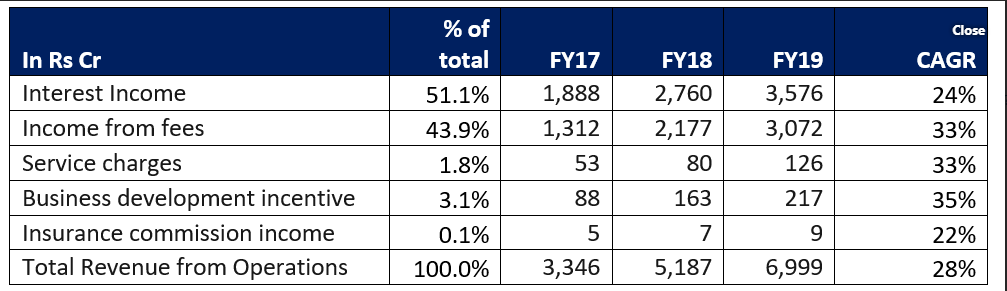

Income From Fees –Income from fees and services is the major component of fee income. These are earned by levying various fees and charges to its cardholders. These can be broken down into three subcategories

Revenues from this category were 44%, 42% and 39% of total revenues in FY19, FY18 and FY17 respectively.

The other sources from where SBI generates revenues in the fee category are

Service Charges – Consists income earned from commission from selling of third party products, brand association fee charged to partners and transaction revenue

Business development incentive income – SBI earns business development incentives from payment networks under long term contracts. The incentives are dependent on increases in credit card spends, cards outstanding and new product launches

Insurance commission income – Income earned by selling insurance products to cardholders

The company also earns other income, these are not from the business operations. These consist primarily of income from investments/FDs, recovery from bad debts written off, liabilities and provisions written back and tax refunds.

SBI card IPO risks

RISKS

The Credit card receivable portfolio falls in the unsecured retail category. Managing credit risk is the holy grail in running a credit card business. We have seen instances in the past where a slow economic growth can severely impact the collections of credit card companies.

This brings us to the question of what are the key factors on which a credit card business thrives? and a slowdown in these factors will hamper the credit card business.

Economic growth and specifical parameters like consumer confidence, unemployment rates, consumer spending and demand for credit are important drivers of a credit card business. The slowdown in any of these will hamper the business, like in 2009 loan defaults had risen due to job losses in the IT and BPO sectors, which heavily impacted unsecured lenders.

Distribution and scale are key factors. A weaker distribution channel will increase costs and in a downturn hurts companies.

Regulations also can spoil the party for credit card companies. For instance, in 2009, there was an RBI guideline that restricted credit card companies from harassing customers for recovery of dues. In addition, recovery agents had to undergo 100 hours of training at IIBF(Indian Institute of Banking and Finance). This slowed down the recovery process.

In the current set up interchange fees for credit cards are not regulated, however, this is not in the case of debit cards. Any move to regulate the interchange fees will impact revenues

Interest rates of credit cards are not regulated and do not move with the interest rates in the market. Interest on revolver loans is high 36-44% and term loans 20-22%, any move to regulate the interest rates that these companies charge will have a severe impact.

The company receivables are short term in nature and its source of funding are commercial paper, non-convertible debentures and working capital loans from banks. Any mismatch between the receivables and the company paying its debt can lead to liquidity risk.

The payment landscape in India is changing. Initiatives like JAM (Jan Dhan, Aadhar and Mobile) have facilitated a move to digital transactions. Demonetization has also lead to people moving towards digital transactions.

There has been an emergence of UPIs and payment wallets, which have helped in moving to a cashless setup. While the selling point of credit card companies in the free credit period (50 days) which these platforms do not offer, we cannot rule out any disruption in this space. We need to keep an eye on the developments in the payment landscape in the country.

UPI volumes in FY19 were 5,353 million as compared to 18 million in FY17. Volumes for H1FY20 stood at 4,966 million. Spends on UPI were Rs 8,770 billion in FY19 as compared to Rs 60 billion in FY17. Spends for H1FY20 was Rs 9,034 billion.

What happened to the Barclays card business?

It was shut down, the performing portfolio was bought by Standard Charted bank and the stressed asset portfolio by Kotak Mahindra bank in 2013.

SBI Card IPO review

Credit card penetration is low in India, companies that have scale and stronger distribution network can expand to smaller cities. Cards issued to NTC (new to credit) customers is growing rapidly. NTC customers are defined as those who have got their bureau record for the first time. NTC customer base has increased by 20% CAGR over the last three years to reach 3 million at the end of FY18.

Payment infrastructure has drastically improved, the payment infrastructure facilitates seamless payments. POS terminals have grown by 27% CAGR from 1.1 million in FY14 to 3.7 million in FY19. It is expected that there would be 5 million POS terminals by 2021. The emergence of payment aggregators/facilitators have also helped.

SBI Cards having a strong parent backing, been in the business for two decades and having a strong distribution channel and scale will certainly benefit from the developments taking place in the payment ecosystem.

The question that we as investors need to ask is – Will we make money by investing in the company? and what are we paying? will the valuation be over the roof?

SBI Card IPO Grey market premium

Reading ET, the grey market premium is believed to be around Rs 200-250 considering IPO price of 600-700.

SBI Card IPO Final verdict

SBI Card is the first IPO in the credit card space. Considering the huge scope of credit cards in India and considering the low penetration levels. It’s a great business to invest in. The current trend in the market is to invest in companies that have a sustaining business model for the future and has a significant market presence. SBI Card IPO qualifies in both of them.

We recommend a SUBSCRIBE to this IPO. Apply for minimum lot size to have a good chance of IPO allocation.

Disclaimer and credits! – All the above facts are obtained from SBI Card DRHP link, Captial minds – https://www.sebi.gov.in/filings/public-issues/dec-2019/sbi-cards-and-payment-services-limited_45160.html

we thanks Gourav Gupta’s(Equialpha.com) answer in Quora link below:-

https://www.quora.com/Is-it-a-good-idea-to-invest-in-an-SBI-card-IPO-Can-an-SBI-IPO-give-good-returns/answers/192053992

Please consult your financial advisor before taking investment descision.

Check Upcoming IPOs in 2020