General Provident Fund (GPF) Latest Interest Rate, Eligibility Criteria, Check Balance, Download GPF Statement Online

The General Provident Fund (GPF) is a popular savings scheme offered by the Indian government to its employees. It is a long-term investment option that provides a secure and guaranteed return on investment, making it an attractive investment option for many. In this article, we will delve deeper into the General Provident Fund in India, its features, benefits, eligibility criteria, and how to download a GPF slip online.

We will also discuss the latest interest rates for GPF and how it compares to other investment options in India. This article will provide you with all the information you need to make an informed decision.

Consider reading: How to check PF Balance Online

Page Contents

General Provident Fund Key Details

| Eligibility | Available to Government employees |

| Investment Period | Till retirement |

| Minimum Contribution | 6% of the basic salary |

| Maximum Contribution | No limit |

| GPF Interest Rate | 7.1% |

| Tax Benefits | Tax-exempt on contributions and interest earned |

| Withdrawal | Partial withdrawals are allowed for specific purposes |

| Loan Facility | Available after 3 years of continuous service |

| Nomination Facility | Available |

| Transferable | Can be transferred between government offices |

Note: The interest rate is subject to change and may vary from year to year. Please check with the relevant authorities for the latest interest rate.

Consider reading: Public Provident Fund (PPF): Features, Benefits and Online Calculator

What is the General Provident Fund (GPF)

The General Provident Fund (GPF) stands as an exemplary government-backed savings scheme in India, tailored specifically for government employees. This scheme is a cornerstone in fostering a financially secure retirement landscape, offering a blend of flexibility, guaranteed returns, and tax advantages.

Voluntary Participation with Seamless Entry and Exit Options: What sets the GPF apart is its voluntary nature, allowing employees the freedom to opt in or out at their convenience. This flexibility ensures that individuals can make decisions best suited to their unique financial circumstances.

Contribution Dynamics: Employee-Government Collaboration: Participation in the GPF involves a systematic contribution process. Employees allocate a portion of their monthly earnings to the fund, a commitment met equally by the government. This matching contribution by the government amplifies the growth potential of the savings.

Compelling Benefits of the General Provident Fund

- Assured and Attractive Returns: The GPF promises a guaranteed return rate, notably surpassing the benchmarks set by many other savings instruments. This assurance of elevated returns makes the GPF an attractive proposition for those seeking reliable growth in their retirement funds.

- Adaptable Contributions for Tailored Savings: Recognizing the diverse financial needs of employees, the GPF offers the liberty to determine the contribution amount. Employees can modify their contributions as per their financial situation, ensuring that the scheme adapts to their evolving savings capacity.

- Tax Efficiency: Maximizing Savings through Tax Deductions: One of the significant advantages of the GPF is its tax-deductible nature. Contributions made towards the fund reduce the taxable income of the employees, translating into substantial tax savings and enhancing the overall appeal of the scheme.

- Unwavering Security Backed by the Government: The backing of the Government of India imbues the GPF with a level of security that is hard to match. This government assurance provides employees with the confidence that their savings are in safe hands, paving the way for a stress-free retirement.

In Summary The General Provident Fund is more than just a savings scheme; it’s a strategic investment in the future for government employees in India. Its combination of flexible contributions, guaranteed returns, tax benefits, and robust security make it an ideal choice for those seeking a stable and prosperous retirement.

Eligibility Criteria for the General Provident Fund (GPF)

Eligibility criteria for the General Provident Fund (GPF):

- Permanent government employees.

- Temporary government employees after a continuous service of one year or more.

- Re-employed pensioners (provided such pensioner is ineligible for Contributory Provident Fund).

- Govt employees who have joined service before 1st Jan 2004.

General Provident Fund (GPF) Rules

As per Ministry Of Personnel, Public Grievances & Pensions Below are the rules for GPF:

- Government employees eligible for the General Provident Fund need to contribute a minimum of 6% of their salary toward GPF.

- The maximum amount an individual can contribute equals 100% of his/her income.

- Contribution to GPF can only be stopped in the case of suspension or retirement.

The Interest Rate for the General Provident Fund (GPF)

The latest GPF Interest Rate is set at 7.1%. In the previous quarter, it was set at 7.9%.

General Provident Fund (GPF) Tax Exemptions

GPF is an EEE tax-free retirement-cum savings scheme. Therefore, the contributions, and interest earned on it as well as the returns from a GPF account are exempt from tax calculations under Section 80C.

Consider reading – EPF vs PPF vs GPF vs VPF

How to Check GPF Balance in India

General Provident Fund (GPF) is a savings scheme for government employees in India. It allows them to contribute a part of their salary every month and earn interest on it. The accumulated amount can be withdrawn at the time of retirement or in case of an emergency.

If you are a government employee and have a GPF account, you might want to check your GPF balance from time to time. This will help you keep track of your savings and plan your future accordingly. Fortunately, there are several ways to check your GPF balance online or offline. Here are some of the methods you can use:

Online Methods to Check GPF Balance in India

- GPF Information and Subscriber’s Login: This is the official website of the Comptroller and Auditor General of India (CAG) that provides GPF information and statements for government employees. You can access this website by clicking here. To check your GPF balance, you need to select your GPF series name, and enter your GPF account number and your PIN number. You will then be able to view your GPF statement, current balance, deposits, withdrawals, interest, etc. You can also download or print your statement for future reference.

- Check Annual GPF Statement of Government Employees of Uttar Pradesh: If you are a government employee of Uttar Pradesh, you can check your annual GPF statement online by visiting this website. You need to enter your GPF account number and click on “View Statement”. You will then see your annual statement for the selected financial year. You can also download or print your statement from this website.

- Other State Websites: If you belong to any other state than Uttar Pradesh, you can check if your state has a dedicated website for providing GPF information and statements. For example, West Bengal has this website where you can check your annual statement of GPF by entering your GPF account number and date of birth. Similarly, other states may have their own websites or portals for GPF services. You can search for them on the Internet or ask your department for the details.

Offline Methods to Check GPF Balance in India

- SMS Alerts: Some states offer SMS alerts for GPF subscribers to inform them about their monthly deposits, withdrawals, interest, balance, etc. For example, Kerala has a service called “GPF SMS Alert” that sends SMS messages to the registered mobile numbers of the subscribers every month. To avail this service, you need to register your mobile number with your department or office. You can also send an SMS to 77362 99997 with the format “GPF <space> <account number>” to get your balance information.

- Missed Call Service: Some states also offer missed call service for GPF subscribers to get their balance information. For example, Tamil Nadu has a service called “GPF Missed Call Service” that allows subscribers to give a missed call to 044-2230 0099 from their registered mobile number and get their balance information through SMS. To avail this service, you need to register your mobile number with your department or office.

- Annual Statement by Post: Another way to check your GPF balance is to wait for the annual statement that is sent by post to your address by the Principal Accountant General (A&E) of your state. This statement shows the opening balance, deposits, withdrawals, interest and closing balance of your GPF account for the financial year. You can also compare this statement with your online statement or SMS alerts to verify the accuracy of the information.

These are some of the methods you can use to check your GPF balance in India. You should always keep an eye on your GPF account and report any discrepancies or errors to your department or office as soon as possible. You should also keep updating your personal details such as address, mobile number, nominee, etc. with your department or office to avoid any inconvenience in the future.

General Provident Fund Rules in India

Here are some of the rules and regulations for the GPF:

- Eligibility: To be eligible for the GPF, employees must be permanent, pensionable employees of the central or state government, or of a local authority or statutory corporation. Employees of semi-government organizations and public sector undertakings may also be eligible for the GPF, depending on their employer’s rules.

- Contributions: Employees who choose to join the GPF must contribute a portion of their monthly salary to the fund. The contribution amount is usually fixed and is determined by the employee’s employer. The government will match the employee’s contribution and will deposit the funds into the employee’s GPF account.

- Withdrawals: Employees are not allowed to withdraw funds from their GPF account until they retire or leave their job. In case of an emergency, employees may be allowed to withdraw funds from their GPF account, but only with the permission of their employer.

- Interest: The GPF offers a guaranteed rate of return, which is higher than most other savings schemes. The interest rate is determined by the government and is revised periodically.

- Tax benefits: Contributions to the GPF are tax-deductible, which means that employees can reduce their taxable income by contributing to the fund. This can result in significant tax savings for employees.

The Advantages and Disadvantages of the General Provident Fund (GPF)

Here are the advantages and disadvantages of the General Provident Fund (GPF) in India:

General Provident Fund (GPF) Advantages:

- Guaranteed returns: GPF provides a guaranteed return on investment, making it a secure option for long-term savings.

- Tax benefits: Contributions to GPF are tax-exempt under Section 80C of the Income Tax Act, 1961, up to a limit of Rs. 1.5 Lakhs per annum.

- Flexible contributions: GPF allows for flexible contributions, with no maximum limit and a minimum contribution of 6% of the basic salary.

- Partial withdrawals: GPF allows for partial withdrawals for specific purposes such as education, housing, and medical expenses.

- Nomination facility: GPF provides a nomination facility, allowing the subscriber to nominate a family member as a beneficiary in case of their untimely demise.

General Provident Fund (GPF) Disadvantages:

- Limited eligibility: GPF is only available to government employees and not to private sector employees or individuals.

- Long-term investment: GPF is a long-term investment option, with a lock-in period till retirement, which may not be suitable for those looking for short-term investments.

- Low-interest rates: The interest rate on GPF is subject to change and may not be as high as other investment options such as mutual funds or stocks.

- No loan facility: GPF does not allow for loans until the subscriber has completed three years of continuous service.

- Limited flexibility: GPF does not allow for the transfer of funds between different investment options or schemes, limiting the flexibility of the investment.

Overall, GPF can be a good investment option for government employees who are looking for a secure long-term savings option with tax benefits. However, it may not be suitable for those looking for more flexibility or higher returns on investment.

It’s important to weigh the advantages and disadvantages of GPF and consider how it fits into your overall investment strategy before making any investment decisions.

Consider using our PPF Online Calculator

Which is better, PPF or GPF?

PPF and GPF offer the same rate of interest. GPF is an easier option for Government employees to contribute towards their savings so it’s a preferred option for them. But looking at the flexibility of withdrawing money and the locking period associated with PPF and GPF, PPF is a better option than GPF.

How to Download Odisha GPF Statement Online

Estimate Cost : INR

Time Needed : 00 days 01 hours 00 minutes

Steps to Download Odisha GPF Slip Online

Visit Odisha General Accountant Page agodisha.gov.in

Visit GPF Odisha portalEnter GPF account number and Provide a registered Password

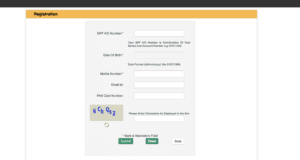

Enter your GPF account number and password if you are already registered. If not then register with your GPF account number. You will need the below details

GPF A/C Number

Date Of Birth

Mobile Number

Email Id

PAN Card NumberSelect the option Account Management form dashboard Menu and Here select Annual Report

select the Account Management option and tap on the Annual reportSelect Year from the center of the page and click Submit

mention year and click the submit option

Tools

- Odisha General Accountant Page agodisha.gov.in

Materials

- GPF Slips online.

FAQs on General Provident Fund (GPF)

What is a General Provident Fund?

The General Provident Fund (GPF) is a mandatory savings scheme available to government employees. It allows them to accumulate funds over the course of their employment through regular contributions from their salary. GPF is a long-term investment option that provides financial security to government employees.

Is GPF and PPF the same?

No GPF is General Provident Fund which is only available for Govt employees. PPF is Public Provident Fund that is available for the general public

How can I access my GPF account?

Different states in India have different GPF portals. You need to go to the corresponding state portal site to access your GPF account.

Is GPF taxable after retirement?

NO. GPF income comes under the EEE category so any income from GPF is completely tax free.

Can I have both GPF and PPF?

Yes, you can have both PPF and GPF accounts if you are a govt employee. If you, are not a govt employee then you can not have a GPF account.

Is GPF eligible for 80c?

Yes. Contribution towards GPF is eligible for

How much can be deposited in GPF?

Government employees eligible for the General Provident Fund can contribute a minimum of 6% of their salary toward GPF, the maximum amount an individual can contribute equals 100% of his/her income.

What is the minimum contribution to GPF?

Government employees eligible for the General Provident Fund can contribute a minimum of 6% of their salary toward GPF.

How to download GPF statements online?

Employees of Govt institutions have to log in to their state GPF portal to download their GPF statement.

How can I check my GPF statement in Karnataka?

Employees of the Karnataka govt can access their GPF account by visiting https://agkar.cag.gov.in/agogpf/ which is the portal for the principal account general Karnataka.

What is the maximum GPF deducted from salary?

The maximum GPF deducted from salary is 5 lakh rupees. If the total contribution is expected to exceed Rs. 5 lakh, the deduction of GPF subscription will be halted once the total contribution reaches the limit in the current financial year. This regulation applies when the minimum monthly subscription of 6% of the emoluments is unable to cover the anticipated contribution.

What is the percentage of GPF contribution?

The percentage of GPF contribution for eligible government employees is a minimum of 6% of their salary, with the option to contribute up to 100% of their income. The only circumstances where contribution to GPF can be stopped are during suspension or retirement. Ensure you stay within these guidelines to maintain your GPF benefits.