National Pension System (NPS) – Returns, Calculator, Tax Benefits, Tier 1, Tier 2, and Annuity in 2023

This post was most recently updated on November 29th, 2023

The National Pension System (NPS) is a government-sponsored retirement savings scheme that has gained popularity among Indian citizens in recent years. It is a voluntary, defined contribution retirement savings plan that is designed to provide financial security during retirement. The NPS offers a range of investment options, including equities, bonds, and government securities, allowing investors to choose the investment mix that aligns with their risk tolerance and financial goals.

In this article, we will explore the features and benefits of the National Pension System in detail, including its investment options, Returns calculator, tax benefits, withdrawal rules, Scheme details, and Annuity.

NPS is an easily accessible, low-cost, tax-efficient, flexible, and portable retirement savings account.

Under the NPS, the individual contributes to his retirement account. NPS is designed on a Defined contribution basis, wherein the subscriber contributes to his own account.

Consider reading: 13 safe investments with high returns in India

Page Contents

National Pension System (NPS) Overview

| Name | National Pension System (NPS) |

| Type | Defined contribution pension system |

| Launch Year | 2004 |

| Regulatory Authority | Pension Fund Regulatory and Development Authority (PFRDA) |

| Eligibility | All Indian citizens between 18 and 65 years of age |

| Contribution | Minimum Rs. 1,000 per year |

| Investment Options | Equity, corporate bonds, government bonds, alternative investment funds |

| Tax Benefits | Up to Rs. 1.5 lakh per year under Section 80C of Income Tax Act, 1961 |

| Withdrawal | Partial withdrawal is allowed after 3 years of account opening; complete withdrawal is allowed after 60 years of age or in case of certain specified medical conditions |

| Annuity | Mandatory purchase of annuity with at least 40% of accumulated corpus on retirement |

| Assets Under Management (AUM) | Rs. 5.78 lakh crore |

| Subscriber Base | 3.6 crore |

| Performance | Average annualized returns of 9.17% (for Tier I accounts) since inception |

Features of National Pension System / NPS Account

The following are the most prominent features of the retirement account under the National Pension System (NPS)

- Every individual subscriber is issued a Permanent Retirement Account Number (PRAN) card which has a 12-digit unique number.

- Under the NPS account, two sub-accounts – Tier I & II are provided. A Tier I account is mandatory and the subscriber has the option to opt for a Tier II account. The following are the features of these sub-accounts:

NPS Tier-I account: This is a permanent retirement account where under which the subscribers have to mandatorily contribute to NPS. Subscribers can withdraw up to 25% of their investment as per exit rules.

NPS Tier-II account: This is a voluntary account that doesn’t have any lock-in. Subscribers of this account can invest and withdraw at any point in time.

Key Advantages of the National Pension System (NPS)

The National Pension System (NPS) in India offers a number of advantages to subscribers:

- Flexibility: The NPS allows subscribers to choose their own investment options and allocation of contributions among different asset classes, such as government securities, corporate bonds, and equity. This allows subscribers to tailor their investments to their own financial goals and risk tolerance.

- Affordability: The NPS has a low minimum contribution requirement, making it accessible to a wide range of individuals.

- Tax Benefits: NPS offers tax benefits, with contributions eligible for tax deductions under Section 80C of the Income Tax Act up to a maximum of INR 1.5 lakhs per year.

- Professional management: The NPS is managed by eight Pension Fund Managers (PFMs), which are experienced investment firms that manage the investment portfolios on behalf of subscribers. This ensures that the investments are managed by professionals with expertise in the financial markets.

- Portability: The NPS account is portable, meaning that it can be transferred from one employer to another or from one PFM to another without any interruption in the service.

- Safety: The NPS is regulated by the Pension Fund Regulatory and Development Authority (PFRDA), which ensures that the funds are managed in a safe and transparent manner.

- Flexibility at retirement: At the time of retirement, NPS subscribers have the option to either withdraw a portion of their balance or purchase an annuity with the balance to receive a regular income during retirement. This allows subscribers to tailor their retirement income to their own needs and preferences.

Key Disadvantages of the National Pension System

The National Pension System (NPS) in India has some potential disadvantages that subscribers should consider before joining:

- Limited investment options: The NPS offers a limited number of investment options compared to other investment products, such as mutual funds or exchange-traded funds (ETFs). This may make it more difficult for subscribers to diversify their portfolios and manage risk.

- Low returns: The NPS has historically had lower returns compared to other investment products, such as mutual funds or equities. This may make it less attractive for investors seeking higher returns on their investments.

- Lack of liquidity: The NPS has restrictions on withdrawing funds before retirement, which may make it less liquid than other investment products. Subscribers are not allowed to make full withdrawals from their NPS account before reaching the age of 60, and partial withdrawals are only allowed for certain specified purposes, such as higher education, buying a house, or medical treatment.

- Complexity: The NPS can be complex and may require a lot of time and effort to understand and manage. Subscribers may need to review and adjust their investments regularly to ensure that they are aligned with their financial goals.

- Lack of flexibility at retirement: The NPS requires subscribers to purchase an annuity with a certain portion of their balance at the time of retirement, which may not be suitable for everyone. This may limit the flexibility of the retirement income options available to subscribers.

Eligibility Criteria for an NPS Account

National Pension System (NPS) accounts can only be opened by Indian citizens including the NRIs aged between 18 to 65 years.

Can I have more than one NPS Account?

No, multiple National Pension System (NPS) accounts for a single individual are not allowed. There is no need to open multiple NPS accounts as NPS accounts are portable via the PRAN.

How and where to open an NPS Account

You can create your National Pension System (NPS) account in 2 ways

- Via POP – Points of Presence

- Via Online

Open an NPS Account Via Points of Presence (POP)

National Pension System (NPS) is distributed through authorized entities called Points of Presence (POP). Almost all the banks (both private and public sector) in India act as Points of Presence under NPS.

To invest in NPS, you are required to open an NPS account through a POP bank, preferably where you have your NRI account.

You can send your NPS application form to your Bank for opening the NPS account.

Open NPS Account Via Online

You can easily create a National Pension System (NPS) account online in 10-20 mins. You can refer to the How to fill NPS form online for step by step guide on how to create an NPS account online.

How to Check the Status of PRAN

If you have applied for National Pension System (NPS) then you can check the status of your PRAN(Permanent Retirement Account Number) by logging into https://cra-nsdl.com/CRA/ using the 17-digit receipt number provided by POP-SP or the acknowledgment number.

Once the PRAN is generated, an email alert, as well as an SMS alert, will be sent to the registered email ID and mobile number of the subscriber.

Documents Required for Opening an NPS Account

The following documents need to be submitted to your Bank (POP) for the opening of a National Pension System (NPS) account:

- Completely filled in the subscriber registration form

- Copy of Passport

- Proof of Address, if the local address is different from the address in your passport.

Can I appoint nominees for the NPS Tier I and Tier II accounts?

Yes, you need to appoint a nominee at the time of opening a National Pension System (NPS) account in the prescribed section of the registration form.

You can appoint up to three nominees in your NPS Tier I and NPS Tier II account.

If you have more than 1 nominee then you are required to specify the percentage of share, which should not be in decimals that you wish to allocate to each nominee.

The share percentage across all nominees should collectively aggregate to 100%.

Can Nominee be Added after the NPS account is created?

If you have not made the nomination to your National Pension System (NPS) account at the time of registration, you can do the same after the allotment of PRAN.

You will have to visit your PoP and place a Service Request to update nominations details. Or you can log in to your NPS account online to update nomination details.

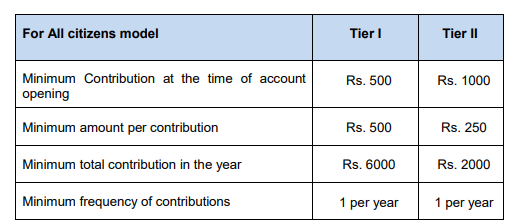

What is the Minimum Contribution for NPS?

The minimum contribution for National Pension System (NPS) depends on the NPS tier.

Funds Managers under NPS

When you invest in National Pension System (NPS), you need to select a pension fund manager who will manage your NPS fund on your behalf of you. It’s like selecting a mutual fund manager for your retirement savings!

At present, there are eight Pension Fund Managers who manage the funds at the option of the subscriber. They are as follows:

- Aditya Birla Sun Life Pension Management Ltd.

- Axis Pension Fund Management Limited

- HDFC Pension Management Co. Ltd.

- ICICI Pru. Pension Fund Mgmt Co. Ltd.

- Kotak Mahindra Pension Fund Ltd.

- LIC Pension Fund Ltd.

- Max Life Pension Fund Management Limited

- SBI Pension Funds Pvt. Ltd

- Tata Pension Management Ltd.

- UTI Retirement Solutions Ltd.

Each PFM manages a variety of pension funds, which are investment portfolios comprising different asset classes such as government securities, corporate bonds, and equity.

Subscribers to the NPS can choose a PFM and a pension fund based on their investment goals and risk tolerance.

It is important for NPS subscribers to carefully consider their investment options and to review their investments regularly to ensure that they are aligned with their financial goals.

You can check their performance here – Best NPS fund manager in 2020 for Tier-1

Different Fund Management Schemes available for NPS

The National Pension System (NPS) provides two methods for investing the subscriber’s funds:

NPS Active Choice: In this strategy, the subscriber themselves selects the asset classes for their fund allocations and the corresponding percentages (with a maximum of 50% for Asset Class E, along with Asset Class C and Asset Class G).

NPS Auto Choice: Known as the Life Cycle Fund, this option is the default under NPS, where the fund’s investment management is automatically conducted based on the subscriber’s age.

As the subscriber ages, the fund’s exposure to Equity (E) and Corporate Debt (C) decreases, while the allocation to Government securities increases to provide a risk mitigation measure.

Is it Possible to Switch Investment Schemes and Fund Managers in NPS?

Yes, it is possible to switch investment schemes and fund managers in the National Pension System (NPS).

As per the guidelines of the Pension Fund Regulatory and Development Authority (PFRDA), subscribers to the NPS are allowed to switch between different investment schemes and fund managers once a year.

The switch can be made online through the subscriber’s NPS account. The NPS offers two investment options – Active Choice and Auto Choice.

Under Active Choice, the subscriber can choose their own asset allocation between equity, corporate bonds, and government securities.

Under Auto Choice, the asset allocation is determined based on the subscriber’s age, with a higher allocation to equities for younger subscribers and a lower allocation for older subscribers.

In addition to the investment options, the NPS also allows subscribers to choose from multiple fund managers, including both public and private sector entities.

Subscribers can switch between fund managers and investment options once a year, subject to certain conditions and limits.

It is important to note that switching investment schemes and fund managers in the NPS may involve certain costs, such as exit loads and transaction fees.

Therefore, subscribers should carefully evaluate their investment needs and goals before making any switch.

It is also advisable to consult with a financial advisor or tax professional to understand the tax implications of switching investment schemes or fund managers in the NPS.

What Income Rax Reliefs are Available for NPS?

The National Pension System (NPS) is a retirement savings scheme that offers tax benefits to encourage individuals to save for their retirement.

Here are the income tax reliefs available for NPS:

- Tax Deduction under Section 80C: Contributions made by an individual to their NPS account are eligible for a tax deduction of up to Rs. 1.5 lakh under Section 80C of the Income Tax Act, 1961. This deduction is also available for contributions made by an individual towards the NPS account of their spouse or children.

- Additional Tax Deduction under Section 80CCD(1B): In addition to the deduction under Section 80C, an individual can claim an additional tax deduction of up to Rs. 50,000 under Section 80CCD(1B) for contributions made towards their NPS account. This means that an individual can claim a total deduction of up to Rs. 2 lakh in a financial year for contributions made toward their NPS account.

- Tax Exemption on Annuity Income: After retirement, when the subscriber purchases an annuity plan with a part of their NPS corpus, the income received from the annuity plan is exempt from tax up to a certain limit. From April 1, 2021, the limit for tax exemption on annuity income has been increased to Rs. 5 lakhs per annum.

- Exemption on Partial Withdrawals: Partial withdrawals made by the subscriber from their NPS account for the treatment of critical illnesses are exempt from tax.

- Tax Treatment of Lump Sum Withdrawals: While 60% of the corpus received at the time of retirement is taxable, the remaining 40% used to purchase an annuity plan is exempt from tax.

These tax benefits make the National Pension System an attractive investment option for individuals looking to save for their retirement while reducing their tax liabilities.

However, it is important to note that tax laws may change from time to time, and subscribers should consult with a tax advisor before making any investment decisions.

NPS Withdrawal Rules

The National Pension System (NPS) is a retirement savings scheme that allows subscribers to accumulate a pension corpus over their working years, which can be used to provide financial security during retirement.

While the primary objective of the NPS is to provide a pension income for subscribers during their retirement years, there are certain conditions under which subscribers are allowed to make partial withdrawals or exit the scheme before the age of retirement.

Here are the withdrawal rules for the National Pension System:

- Normal Exit: When a subscriber reaches the age of 60, they are required to use a part of their NPS corpus to purchase an annuity plan, which provides a regular pension income for the rest of their life. The subscriber is allowed to withdraw up to 60% of the remaining corpus as a lump sum at the time of retirement. The remaining 40% of the corpus must be used to purchase an annuity plan.

- Early Exit: In case of an early exit before the age of 60, the subscriber is allowed to withdraw up to 20% of the accumulated corpus as a lump sum. The remaining 80% of the corpus must be used to purchase an annuity plan.

- Partial Withdrawals: Subscribers are allowed to make partial withdrawals from their NPS account during their working years for specific purposes such as higher education, marriage, purchase or construction of a house, or for the treatment of critical illnesses. Subscribers can make a maximum of three partial withdrawals during the entire tenure of the scheme, subject to certain conditions and limits.

- Death of Subscriber: In case of the subscriber’s death, the entire accumulated corpus is paid to the nominee or legal heirs. The nominee can choose to receive the corpus as a lump sum or a pension income, subject to certain conditions and limits.

It is important to note that partial withdrawals from NPS accounts are taxable unless they are made for the treatment of critical illnesses.

Therefore, subscribers should carefully evaluate their financial needs and the tax implications before making any partial withdrawals from their NPS account.

What are NPS Partial Withdrawal rules?

You can do partial withdrawal of the National Pension System(NPS) only in the below scenarios:

- For the purpose of higher education of his/her children,

- For the marriage of his/her children,

- For the purchase or construction of a residential house or flat

- For treatment of specified illnesses.

How many Partial Withdrawals are Allowed in NPS?

Under the National Pension System (NPS), subscribers are allowed to make partial withdrawals from their NPS account for specific reasons. These partial withdrawals are allowed only under certain conditions and are subject to certain limits.

As per the NPS guidelines, subscribers are allowed to make a maximum of three partial withdrawals during the entire tenure of the scheme. The withdrawals can be made after the completion of three years of opening the NPS account and are subject to certain conditions.

The first partial withdrawal of up to 25% of the subscriber’s contributions is allowed only for specific purposes, such as higher education, marriage, purchase or construction of a house, or for treatment of critical illnesses.

The second and third partial withdrawals of up to 25% each are allowed only after a gap of at least five years from the previous withdrawal and are subject to certain conditions.

The second and third withdrawals can be made only for specific purposes, such as children’s marriage, higher education, or for the treatment of critical illnesses of the subscriber, spouse, children, or dependent parents.

It is important to note that partial withdrawals from NPS accounts are taxable unless they are made for the treatment of critical illnesses. Therefore, subscribers should carefully evaluate their financial needs and the tax implications before making any partial withdrawals from their NPS account.

Annuity under NPS

An annuity is a financial product that provides a regular income stream in exchange for a lump sum payment. In the context of the National Pension System (NPS), annuity refers to the pension payments that an individual receives during retirement.

After an individual reaches the age of 60, they are required to use a part of their NPS corpus to purchase an annuity from a registered life insurance company.

The annuity provides a regular income stream to the annuitant for the rest of their life.

Annuity options under National Pension System (NPS) include:

- Life annuity: This provides a regular income stream for the annuitant’s life, and the payments stop upon the annuitant’s death.

- Joint life annuity: This provides a regular income stream for the annuitant and their spouse, and the payments continue to the surviving spouse after the annuitant’s death.

- Increasing annuity: This provides a regular income stream that increases every year, typically to keep up with inflation.

- Annuity certain: This provides a regular income stream for a fixed period, typically 5, 10, or 15 years, regardless of whether the annuitant is alive or not.

The annuity rates under NPS are determined by the life insurance companies and are subject to change based on market conditions.

An individual can choose the annuity option that best suits their financial needs and retirement goals.

It is important to note that once an individual purchases an annuity, the decision is irreversible, and they cannot change the annuity option or the life insurance company.

Therefore, it is crucial to carefully evaluate the options and choose the one that aligns with their financial goals and retirement needs.

For the latest update on NPS please visit https://npscra.nsdl.co.in/

Final Thought on National Pension System

Navigating the world of retirement planning, the National Pension System (NPS) emerges as a pivotal component in India’s financial framework.

As a long-term retirement savings scheme, NPS offers a blend of equity, fixed deposits, corporate bonds, liquid funds, and government funds, allowing subscribers to optimize returns based on their risk appetite.

The dual benefits of substantial tax savings coupled with a disciplined approach to retirement planning make NPS a noteworthy consideration for every Indian. As with any financial instrument, diving deep into its intricacies ensures that one harnesses its full potential.

FAQs on National Pension System (NPS)

What is National pension system?

The national pension system (NPS) is a market-linked, defined contribution product. It offers two types of accounts, Tier-I and Tier-II. Each subscriber is assigned a unique Permanent Retirement Account Number (PRAN), maintained by the Central Recordkeeping Agency (CRA). NPS allows individuals to save for retirement effectively.

What is NPS and its benefits?

NPS, or National Pension System, offers various benefits. It allows you to invest in asset classes like equity, bonds, and government securities to diversify your investments. Additionally, NPS provides tax benefits of up to 2 Lakhs under three provisions: 80CCD(1), 80CCD(1B), and 80CCD(2). Take advantage of NPS to enjoy tax benefits and choose from a range of investment options.

Who is eligible to join the NPS in India?

In India, the NPS is open to all citizens of India, including self-employed individuals, salaried employees, and the unorganized sector. However, the NPS is not available to non-resident Indians (NRIs).

What are the tax benefits of the NPS in India?

The NPS offers several tax benefits in India. Contributions to the NPS are eligible for tax deductions under Section 80C of the Income Tax Act, up to a maximum of INR 1.5 lakhs per year. In addition, contributions made by an employer are eligible for a tax deduction under Section 80CCD (2) up to INR 50,000 per year. The annuity income received from the NPS at the time of retirement is also tax-free up to a certain limit.

What are the investment options available under the NPS in India?

Under the NPS in India, you can choose to invest your contributions in a variety of asset classes, including government securities, corporate bonds, and equity. You can also choose to allocate your investments among these asset classes in a way that aligns with your risk tolerance and investment goals.

Can I withdraw from my NPS account in India before retirement?

Under the NPS in India, you can make partial withdrawals from your account for certain specified purposes, such as higher education, buying a house, or medical treatment. However, you are not allowed to make full withdrawals from your NPS account before reaching the age of 60. At the age of 60, you can choose to either withdraw a portion of your NPS balance or purchase an annuity with the balance to receive a regular income during retirement.

How much pension will I get in NPS?

The amount of pension you will receive in NPS depends on various factors such as your contributions, years of service, and market performance. To calculate an estimate, you can use an NPS calculator. Simply input your details and it will provide you with an approximate pension amount. Make sure to consult with a financial advisor for personalized advice.

How can I get 50,000 pension per month in NPS?

To receive a monthly pension of INR 50,000 through NPS, you can invest INR 11,000 annually for 30 years. Assuming a 10% investment rate, the total accumulated investment would be over INR 2.5 Crores. At maturity, allocate 40% of the corpus towards purchasing an annuity plan, which will provide the desired monthly pension.