Voluntary Provident Fund (VPF) – Latest Interest Rate, Returns, Rules and Regulations

This post was most recently updated on November 29th, 2023

The voluntary Provident Fund (VPF) is an extension of the Employee Provident Fund (EPF), which allows salaried employees to contribute more than the mandatory contribution towards their retirement savings. It is a popular long-term investment option in India, offering a secure and guaranteed return on investment.

In this article, we will delve deeper into the Voluntary Provident Fund, the latest interest rate, features, benefits, withdrawal rules, and interest rate history.

We will also provide a free VPF Returns Calculator to help you calculate your returns.

Consider reading: Public Provident Fund (PPF)

Page Contents

Voluntary Provident Fund Key Details

| Eligibility | Available to salaried employees who are contributing to EPF |

| Investment Period | 5 years (minimum) |

| Minimum Contribution | Basic salary + dearness allowance |

| Maximum Contribution | No limit (subject to the basic salary and dearness allowance) |

| Interest Rate | 8.1% (as of 2022-23) |

| Tax Benefits | Tax-exempt on contributions, interest earned, and maturity proceeds |

| Withdrawal | Partial withdrawals are allowed after the completion of 5 years |

| Loan Facility | Available from the 3rd to the 6th year |

| Nomination Facility | Available |

| Transferable | Can be transferred from one employer to another |

Note: The interest rate is subject to change and may vary from year to year. Please check with the relevant authorities for the latest interest rate.

Additionally, VPF contributions are made by the employee and not the employer and the contributions are deducted from the employee’s salary. The interest earned on VPF is compounded annually, providing higher returns over the long term.

VPF is a safe investment option, backed by the Government of India, and offers a good balance of risk and return.

Consider reading: Online PPF Returns Calculator

What is a Voluntary Provident Fund (VPF)?

A Voluntary Provident Fund (VPF) is a voluntary fund contribution from the employee towards his/her provident fund account. This contribution is beyond the 12% contribution by an employee towards his EPF.

The maximum contribution is up to 100% of his Basic Salary and Dearness Allowance. Interest is earned at the same rate as the EPF. VPF is managed by EPFO

Consider reading – 13 safe investments with high returns in India

Who can Invest in Voluntary Provident Fund?

VPF is an extension of the EPF. The VPF option is available only to salaried individuals who receive their monthly salary payments through a specific salary account and contribute to EPF.

What are the Benefits of the Voluntary Provident Fund?

There are many benefits of VPF.

1. Excellent Tax Saver via the EEE category

The VPF falls under the EEE category ( EEE – exempt on contribution; exempt from the principal; exempt on interest) making it an excellent tax-saving option.

2. Safe Investment Option

The scheme is managed by EPFO under the Govt of India undertaking with a fixed interest rate. Hence, it is considered a risk-free investment.

3. Easy to Apply

Salaried employees can use their EPF account for contributions as part of their VPF investment. They can just simply contact their salary department to mention the amount they want to contribute toward the VPF.

4. High Returns than PPF

Currently, the interest for EPF / VPF is accrued at 8.10% per annum under this scheme. Contributions up to 1.5 lakhs PA and interest accrued are exempt from tax under Section 80C, resulting in higher returns from a long-term perspective.

VPF offers higher returns than PPF as it is part of EPF.

Consider reading – Income tax exemptions and deductions available for salaried employees

5. Easily Transferable

Just like EPF, It is really easy to transfer the VPF account(part of the EPF account) when you switch jobs as the UAN reference remains unique for a subscriber.

What are the Withdrawal Rules for the Voluntary Provident Fund?

You can do a partial withdrawal of VPF as a loan. If the withdrawal was made before 5 years you need to pay taxes for the interest earned for the 5-year period. The interest income gets added to the total income.

In case of resignation or termination from service: When the employee either resigns or gets terminated from service then the final maturity amount is paid to him/her.

In case of death while in service: In case of the untimely death of the VPF subscriber, the VPF amount is paid to the nominee of the subscriber. If there is no nominee for the EPF/VPF account then the amount is paid to the legal heir of the subscriber.

The VPF fund is mainly popular as the accumulated money can be withdrawn at any given time. You can withdraw from the VPF account for any of the reasons mentioned below:-

- Payments of medical bills for the individual and his kin

- Cost-intensive events like higher education and marriage

- Payments for house construction or purchase of new land/house

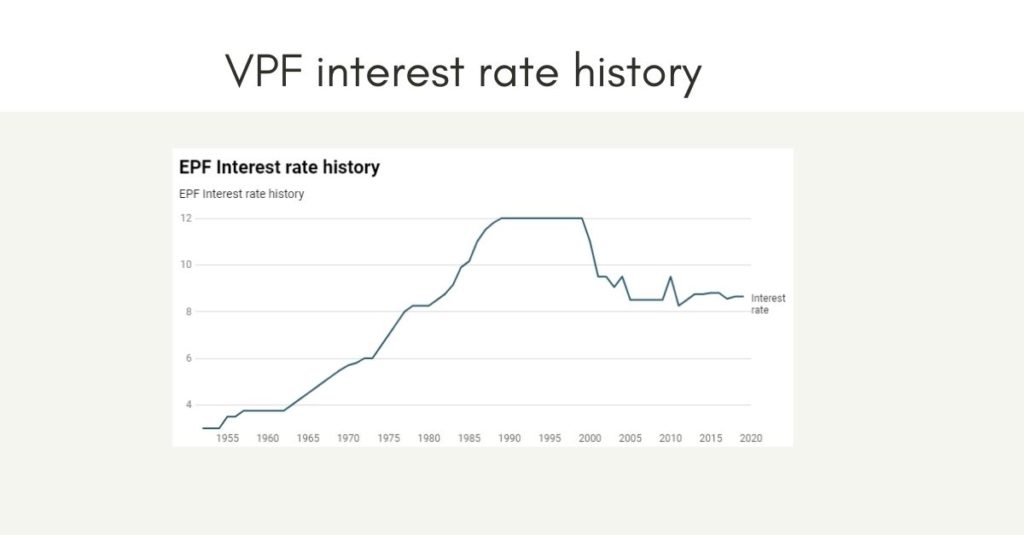

VPF Interest Rate History

Since VPF has the same interest as EPF; below is the interest history for EPF / VPF:

Advantages and Disadvantages of Voluntary Provident Fund

Sure, here are the advantages and disadvantages of the Voluntary Provident Fund (VPF) in India:

Advantages:

- Guaranteed returns: VPF provides a guaranteed return on investment, making it a secure option for long-term savings.

- Tax benefits: Contributions to VPF are tax-exempt under Section 80C of the Income Tax Act, 1961, up to a limit of Rs. 1.5 Lakhs per annum. The interest earned on VPF is also tax-exempt, and the maturity proceeds are also tax-free.

- Flexible contributions: VPF allows for flexible contributions, with no maximum limit and a minimum contribution of the employee’s basic salary and dearness allowance.

- Higher returns: The interest rate on VPF is typically higher than other fixed-income investment options, providing higher returns over the long term.

- Retirement benefits: VPF provides a significant retirement corpus, which can be used to support the employee’s post-retirement lifestyle.

Disadvantages:

- Limited liquidity: VPF is a long-term investment option, with a lock-in period of five years. Partial withdrawals are not allowed before the completion of five years.

- No loan facility: VPF does not allow for loans until the subscriber has completed three years of continuous service.

- Dependence on the employer: VPF contributions are made by the employee and not the employer, but the employer plays a crucial role in facilitating VPF contributions and managing the account. Any issues with the employer or company can affect VPF contributions and returns.

- Interest rate changes: The interest rate on VPF is subject to change and may not be as high as expected, depending on market conditions.

Overall, VPF can be a good investment option for salaried employees looking to maximize their retirement savings and achieve higher returns over the long term.

Voluntary Provident Fund (VPF) Calculator

Here is the Free Voluntary Provident Fund (VPF) Calculator:

Final Thoughts on Voluntary Provident Fund

As an active investor, I highly recommend Voluntary Provident Fund (VPF) as a smart long-term investment option for salaried employees in India.

VPF provides a guaranteed return on investment, with a high-interest rate, tax benefits, and flexible contributions.

It’s a secure investment option, backed by the Government of India, and can provide a significant retirement corpus for employees.

However, it’s important to consider the advantages and disadvantages of VPF before making any investment decisions.

While VPF provides higher returns and tax benefits, it also has limited liquidity, dependence on the employer, and interest rate changes.

If you’re a salaried employee looking to maximize your retirement savings and achieve higher returns over the long term, VPF could be the right investment option for you. It’s important to carefully consider your financial goals, investment horizon, and risk appetite before making any investment decisions.

In summary, VPF is a highly recommended investment option for salaried employees in India who are looking for a secure and guaranteed return on investment with tax benefits.

Consider reading: Top 10 Best Investment Options in India

FAQs on Voluntary Provident Fund (VPF)

What is voluntary provident fund?

The Voluntary Provident Fund (VPF), or voluntary retirement fund, is an additional, optional contribution that employees can make towards their Provident Fund (PF) account, beyond the mandatory 12% contribution to the Employee Provident Fund (EPF). Employees can contribute up to 100% of their basic salary and dearness allowance.

Who is eligible for VPF?

Salaried employees with an active EPF account and a monthly salary deposited into their salary account can invest in VPF. To check eligibility, individuals should ensure they meet these criteria.

How to check the balance in the VPF account?

You can check your VPF passbook along with your EPF passbook here: https://passbook.epfindia.gov.in/MemberPassBook/Login

Is VPF a good investment?

VPF is excellent if you are looking for safe and secure returns which is better than normal bank fixed deposits.

Is VPF better than PPF?

Yes VPF is better than PPF is you are a salaried employee and contribute to EPF. VPF gives a higher rate of interest compared to PPF. PPF currently offers a 7.1% interest rate but VPF offers an 8.65% interest rate in July 2020. Also, You can withdraw your amount in VPF along with your EPF investments, unlike EPF where you have a lock-in period of 15 years.

Which is better NPS or VPF?

NPS and VPF are investment options targeted for retirement. NPS offers subscribers to opt for equity options as part of fund selection which gives higher returns over the long term. VPF offers safe and stable returns consistently.

So if you are near your retirement then it is best to stick to VPF for your investments but if you have a longer retirement time then NPS will be a better choice for you.Is VPF exempted from tax?

Yes VPF contributions can be claimed as part of 80C tax exemptions. Also, any gains from VPF is exempted from tax as per the EEE mechanism.

Where can I open a VPF account?

You don’t need to create a separate account for VPF. You can request your employer to add your VPF contributions to your existing EPF account.

Is VPF better than mutual funds?

VPF is a stable high yield fixed returns instrument that gives higher returns with EEE tax benefit but over the long term (10+ years) equity mutual funds have given far better returns than VPF so if your time horizon is less than 10 years then stock to VPF otherwise look for investments in equity mutual funds.

What is the latest VPF interest rate in 2023?

8.10% is the VPF interest rate as of July 2023.

What is the latest PPF interest rate in 2023?

7.10% is the PPF interest rate as of July 2023.

How much VPF is good?

A good amount for VPF contribution is over and above the PF limit of 12%. However, there is no specific requirement for the employee to contribute a particular amount. The employee can contribute their entire basic salary and dearness allowance to the VPF account. Strive to maximize contributions based on individual financial goals and circumstances.