Are debt funds safe? which debt funds to invest in in 2023?

Are debt funds safe? – With the recent episode of Franklin Templeton AMC winding up 6 of its debt funds, every retail investor has a question in their mind – are debt funds safe to invest in?

Normally debt funds are marketed by MF distributors as a very safe investment product. They are meant to protect the customers from the equity MF type of risk where in equity MF the investors can lose a lot of money.

But with the recent events it’s looking like the debt funds are more riskier than equity funds as there is a hope of recovery in equity MF but when a company defaults on its payments to a debt mutual fund then debt mutual fund NAV takes a hit and never recovers!

It all started in September 2018 when IL&FS defaulted on its payments to the Small Industries Development Bank of India. Slowly the debt funds started writing down their investments in DHFL, Vodafone idea, Yes bank, etc.

With Yes bank’s default a lot of debt mutual funds took a large hit to their NAVs, and some of their funds have taken a hit of up to 25% on their NAVs. No retail investor in their wildest dreams would have imagined that their debt mutual fund investment can go down by 25%!

Page Contents

So why did this happen with debt funds?

Some fund houses have invested in commercial papers of companies that initially were rated excellent by rating agencies but they later turned out to be junk investments and these funds had to write down their investments in those companies. Eventually leading to investors losing their money.

The fund houses were investing in those companies in a hope of higher returns and beating their counterparts in other AMCs. This worked well till 2018 as companies didn’t default till then. Franklin Templeton AMC was among the best debt fund AMC till 2018.

With defaults, they started giving negative returns!

After Vodafone Idea defaults, Franklin Templeton AMCs 6 funds have given a massive decline in their NAVs in a single day. These are the 6 funds that were winded up on 23rd April 2020. Maybe the warning signs were already there for the investors to exit!

Do read – Franklin Templeton debt funds- What went wrong?

Are debt funds safe – If yes, Which ones?

There are so many types of debt funds available in the market. They serve different purposes and they invest in different instruments.

It’s very difficult for a normal retail investor to know which debt fund is safe for them out of so many options.

Let’s do an analysis of all the debt funds available in the market and see their performance over the years. We will do the analysis of the funds which are in the market for at least 5 years.

What are Debt Funds?

Debt funds are a type of mutual fund that invests in fixed-income securities such as corporate bonds, government bonds, and money market instruments. They aim to generate income for investors through the interest earned on these securities. Debt funds are considered to be less risky than equity funds, as the value of the underlying securities is typically more stable.

Debt funds are a popular investment option in India, as they offer the potential for a steady income and are less volatile than equity funds. They are suitable for investors who have a moderate to low-risk tolerance, and who are looking to diversify their portfolio and generate a regular stream of income.

Debt funds can be classified based on the maturity of the underlying securities, with money market funds investing in short-term instruments, short-term debt funds investing in instruments with maturities of up to three years, and long-term debt funds investing in instruments with maturities of more than seven years. There are also specialized debt funds that invest in specific types of securities, such as government bonds (gilt funds) or corporate bonds (corporate bond funds).

Types of Debt Funds available in India

There are several types of debt funds available in India, including:

- Money market funds: These funds invest in short-term debt instruments such as commercial paper and certificates of deposit, with maturities of up to one year. Money market funds are considered to be the least risky type of debt fund.

- Short-term debt funds: These funds invest in debt instruments with maturities of up to three years. They are considered to be slightly riskier than money market funds, but still relatively low risk.

- Medium-term debt funds: These funds invest in debt instruments with maturities of three to seven years. They have a moderate level of risk.

- Long-term debt funds: These funds invest in debt instruments with maturities of more than seven years. They are considered to be the riskiest type of debt fund, as the value of the underlying securities is more susceptible to fluctuations in interest rates.

- Gilt funds: These funds invest exclusively in government securities, including bonds issued by the central and state governments. Gilt funds are considered to be low risk, as the risk of default is low for government bonds.

- Floating rate funds: These funds invest in debt instruments with floating interest rates, which means that the interest rate on the securities adjusts based on changes in market rates. Floating rate funds are designed to protect against interest rate risk.

- Corporate bond funds: These funds invest in corporate bonds issued by companies. They are considered to be slightly riskier than government bond funds, as there is a higher risk of default.

- Income funds: These funds invest in a mix of debt and equity securities, with the aim of generating income for investors. Income funds are considered to have a moderate level of risk.

- Dynamic bond funds: These funds invest in a mix of debt instruments with different maturities, and actively adjust the portfolio based on the fund manager’s market outlook. Dynamic bond funds are considered to have a moderate level of risk.

Advantages and Disadvantages of investing in Debt Funds in India

Here are some advantages and disadvantages of investing in debt funds in India:

Advantages:

- Potential for higher returns: Debt funds typically have the potential to generate higher returns compared to bank deposits and savings accounts.

- Professional management: Debt funds are managed by professional fund managers who have expertise in selecting high-quality debt instruments and optimizing the portfolio for maximum returns.

- Diversification: Debt funds offer the opportunity to diversify your investment portfolio, as they invest in a wide range of debt instruments.

- Liquidity: Most debt funds offer the option to redeem your investment on any business day, providing you with the flexibility to withdraw your money when you need it.

Disadvantages:

- Risk of default: The credit quality of the debt instruments held in the fund will determine the risk of default. A debt fund that invests in low-quality or high-risk debt instruments is more vulnerable to default risk.

- Interest rate risk: Changes in interest rates can affect the value of the debt instruments held in the fund. If interest rates rise, the value of the fund’s holdings may decline, and vice versa.

- Inflation risk: Debt fund returns may not keep pace with inflation, which can erode the purchasing power of your investment over time.

- Taxation: The taxation treatment of debt fund gains depends on the holding period. Short-term gains (held for less than 3 years) are taxed as per the investor’s income tax slab, while long-term gains (held for more than 3 years) are taxed at 20% after factoring in indexation benefits.

Let’s look at the details of each type of Debt fund available in India:

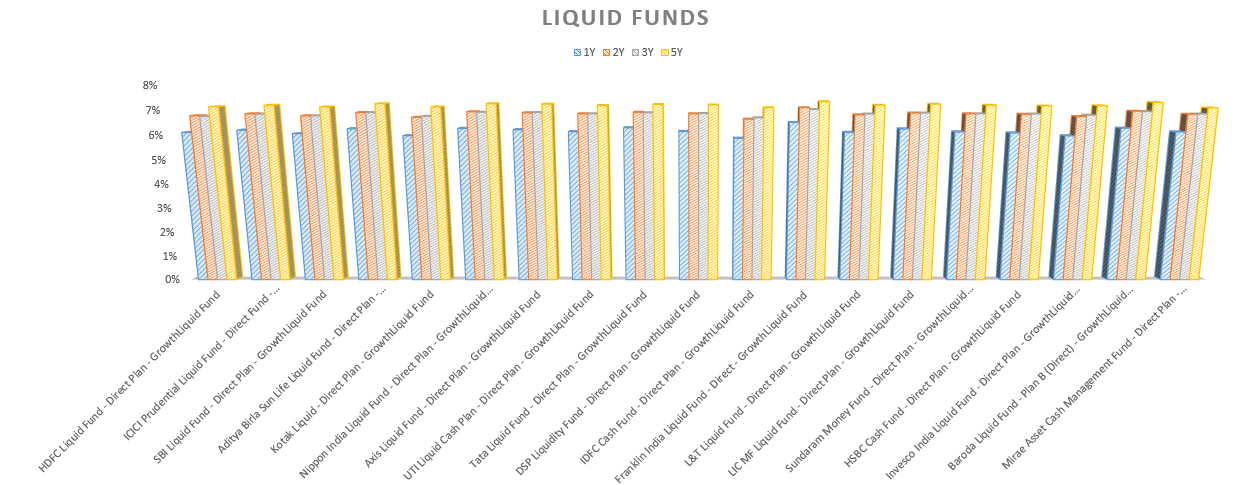

Liquid funds

Liquid funds invest in bonds having a maturity of up to 3 months. They are suitable to park the amount that you have set aside to meet any emergency needs or any surplus money that you don’t need for the next few months to a year. You can expect to earn better returns than what you would get from a bank account.

The risk of incurring a loss in these funds is negligible but they do not guarantee returns or the safety of capital. Though rare, there have been few instances when liquid funds have incurred losses.

Performances of liquid MFs over the last 5 years:

Should retail investors invest in liquid funds? – Yes. Stick to the large liquid funds.

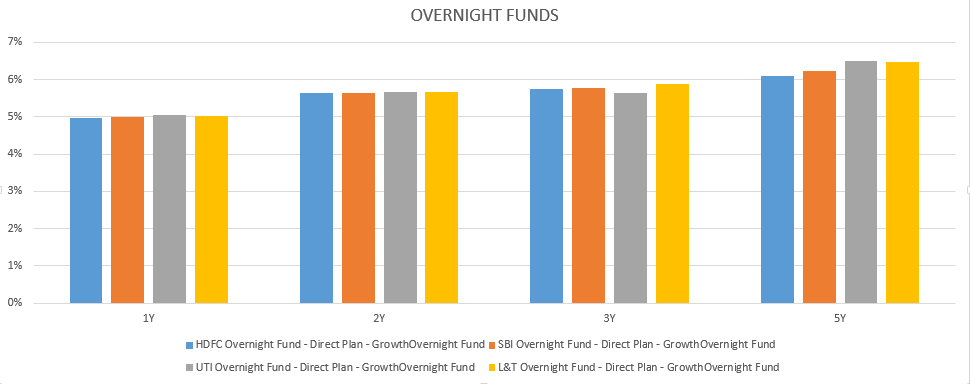

Overnight funds

Overnight funds invest in bonds having a maturity of just one day (hence the name ‘Overnight’). They are suitable for institutional investors looking to park their surplus money for a few days or weeks to earn a bit extra on the sum which would otherwise lie idle in a bank account. The risk of incurring a loss in these funds is negligible but they do not guarantee returns or the safety of capital.

Performances of Overnight MFs over the last 5 years:

Should retail investors invest in overnight funds? Yes. If you don’t want to trust liquid funds and don’t want to risk your money at all. Liquid funds are better than overnight funds in terms of returns.

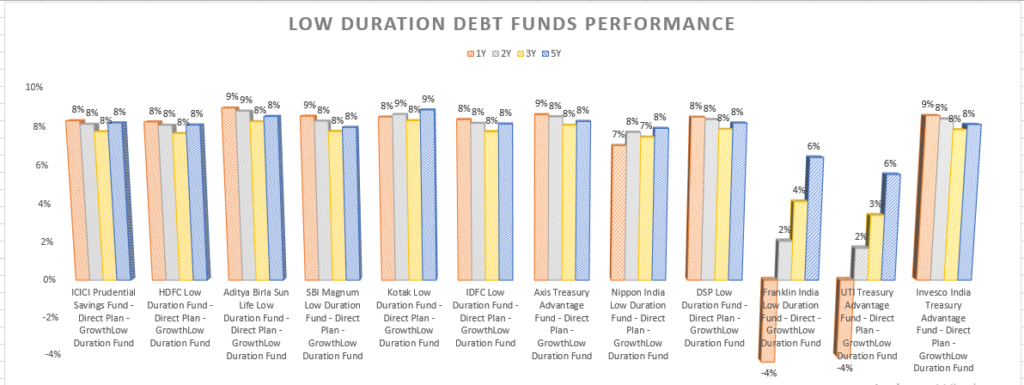

Low duration funds

Low Duration debt funds invest in bonds maturing in 6 months to 1 year time. They aim to earn slightly better returns than what you can get from a bank account or a short-duration fixed deposit. The risk of incurring a loss in these funds is negligible but they do not guarantee returns or the safety of capital.

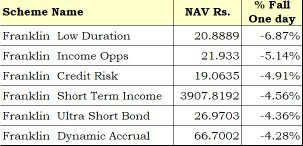

Since these funds invest in different categories of companies there is a high chance of defaults if the AMC has invested in a company that doesn’t pay the money back. If you see the below chart; there are funds that have given negative returns in these categories.

Performances of low-duration MFs over the last 5 years:

Should retail investors invest in low-duration funds?

- Yes- only if you can examine the investments of your fund

- No – If you don’t understand how the fund invests your money

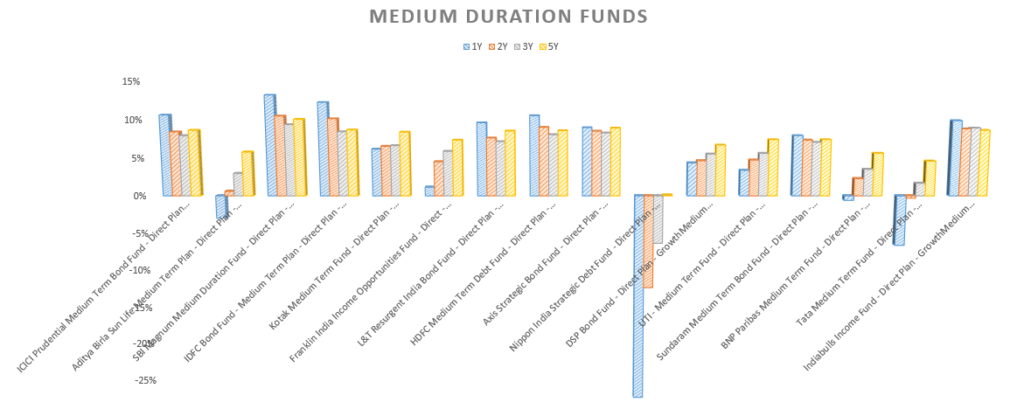

Medium duration funds

Medium Duration debt funds invest in bonds maturing in 3 to 4 years time. They aim to earn slightly better returns than inflation and bank fixed deposits of a similar duration. The risk of incurring a loss in these funds over the said time frame is low, but they do not guarantee returns or the safety of capital.

Since these funds invest in a different category of companies there is a high chance of defaults if the AMC has invested in a company that doesn’t pay the money back. If you see the below chart; there are funds that have given negative returns in these categories.

Performances of medium-duration MFs over the last 5 years:

Should retail investors invest in medium-duration funds?

- Yes- only if you can examine the investments of your fund

- No – If you don’t understand how the fund invests your money

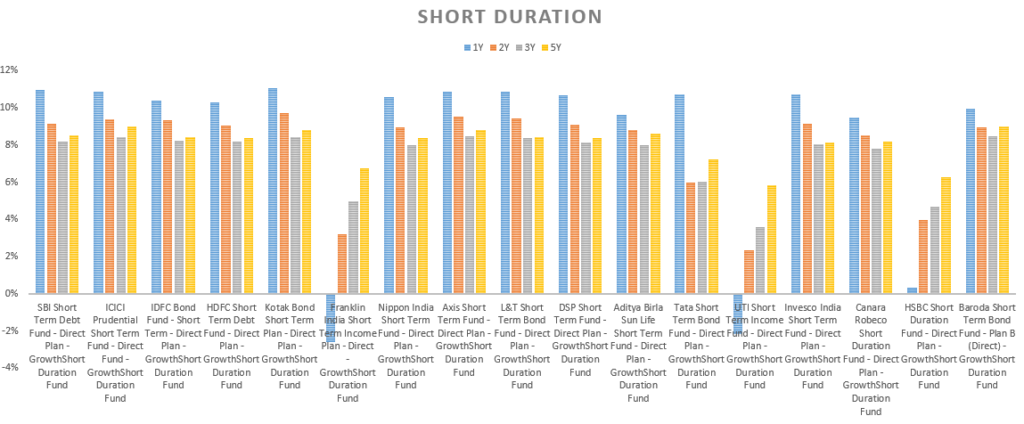

Short duration funds

Short Duration debt funds are suitable to invest your money for a duration of 1 year to 3 years. You can expect to earn higher returns than what a bank fixed deposit of a similar duration can fetch.

The risk of incurring a loss in these funds over the said time frame is low, but they do not guarantee returns or the safety of capital like a bank deposit. There have been instances when short-duration funds have incurred losses.

Since these funds invest in a different category of companies there is a high chance of defaults if the AMC has invested in a company that doesn’t pay the money back. If you see the below chart; there are funds that have given negative returns in these categories.

Performances of short-duration MFs over the last 5 years:-

Should retail investors invest in short-duration funds?

- Yes- only if you can examine the investments of your fund

- No – If you don’t understand how the fund invests your money

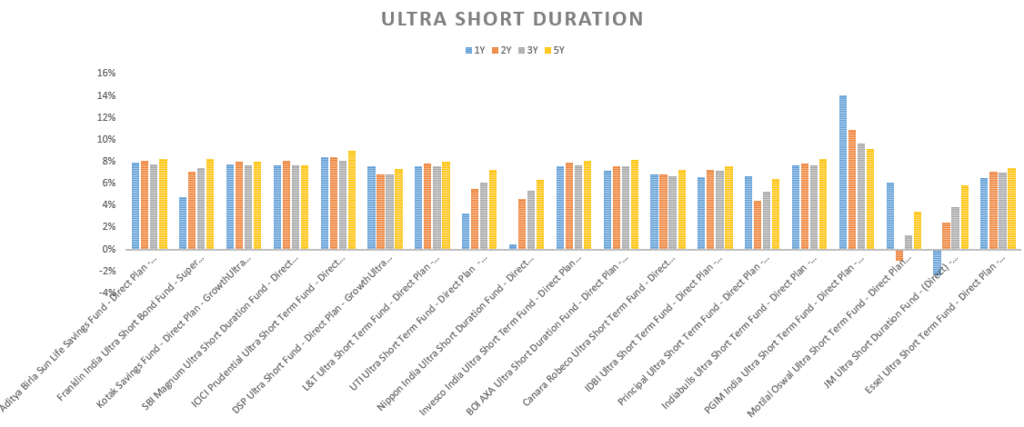

Ultra short-duration funds

Ultra Short Duration debt funds invest in bonds maturing in 3 to 6 months’ time. They aim to earn slightly better returns than what you can get from a bank account or a short-duration fixed deposit. The risk of incurring a loss in these funds is negligible but they do not guarantee returns or the safety of capital.

Since these funds invest in a different category of companies there is a high chance of defaults if the AMC has invested in a company that doesn’t pay the money back. If you see the below chart; there are funds that have given negative returns in this category.

Performances of Ultra short duration MFs over the last 5 years:

Should retail investors invest in Ultra Short duration funds?

- Yes- only if you can examine the investments of your fund

- No – If you don’t understand how the fund invests your money

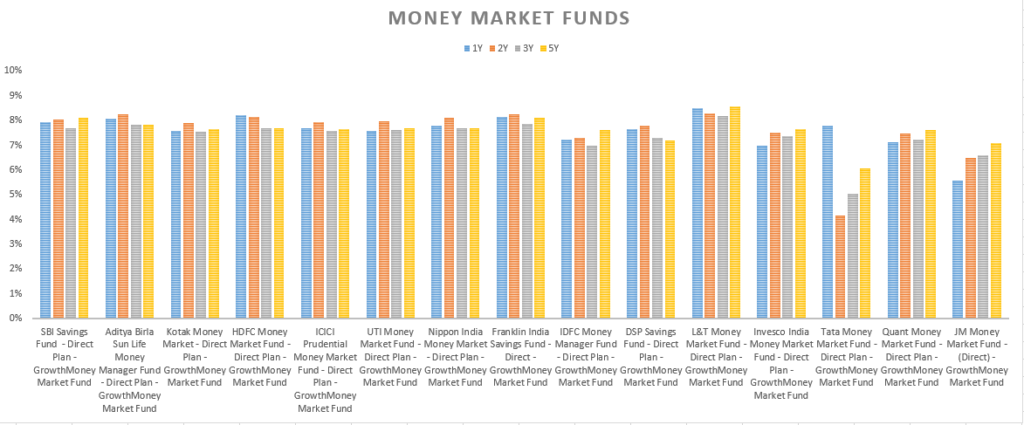

Money Market funds

Money Market debt funds invest in bonds with a maturity of up to 1 year. They aim to earn slightly better returns than what you can get from a bank account or a short-duration fixed deposit. The risk of incurring a loss in these funds is negligible but they do not guarantee returns or the safety of capital.

Performances of Money market MFs over the last 5 years:

Should retail investors invest in Money market funds:

Yes- although no funds have given negative returns in this category. The returns of this category is almost the same as liquid funds. So retail investors are better off sticking to liquid funds.

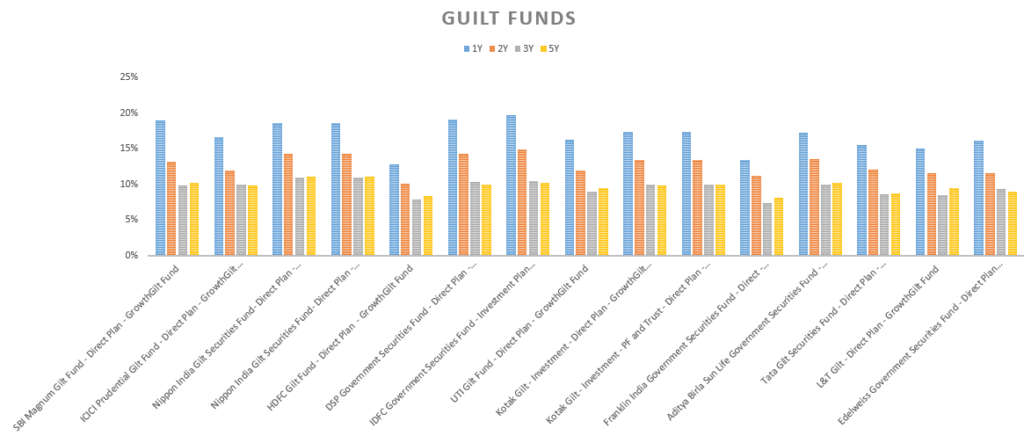

Gilt Funds

This is a fund that invests mainly in bonds issued by the government of India. These bonds do not carry any risk of default since the repayment of investors’ money is backed by the government. But they are prone to sharper ups and downs because of changes in interest rates.

Performances of Gilt MFs over the last 5 years:

Should retail investors invest in Gilt funds –

Yes- in an existing scenario where the interest rate is heading downward and bond yields are going down. Remember these funds can give negative returns when the bond yields start rising up!

If you see there is a spike in returns for this year as the bond yields have crashed this year!

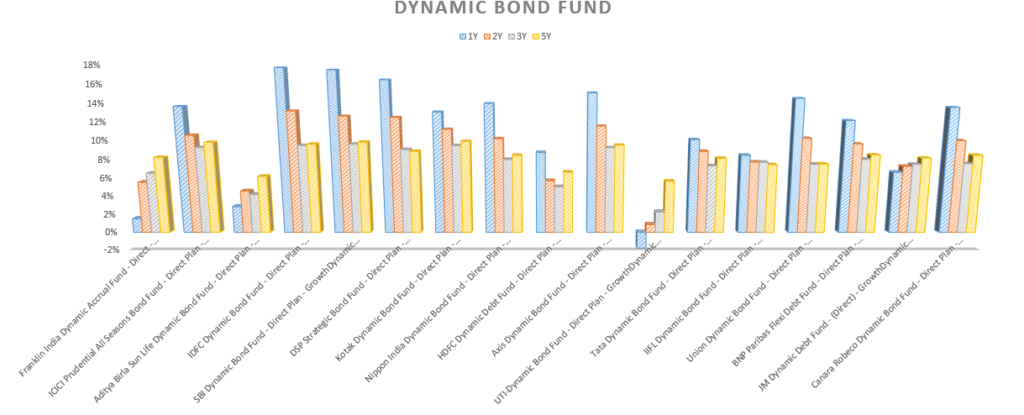

Dynamic Bond fund

Dynamic Bond funds have the freedom to invest in bonds of any duration. Depending upon where it expects to earn maximum returns, the fund management team decides whether to invest in bonds maturing in a few months’ time or in the ones maturing several years later.

Therefore, they are the most versatile type of debt funds available.

Since these funds invest in a different category of companies there is a high chance of defaults if the AMC has invested in a company that doesn’t pay the money back. If you see the below chart; there are funds that have given negative returns in this category.

Performances of Dynamic bond MFs over the last 5 years:

Should retail investors invest in Dynamic bond funds?

- Yes- only if you can examine the investments of your fund

- No – If you don’t understand how the fund invests your money

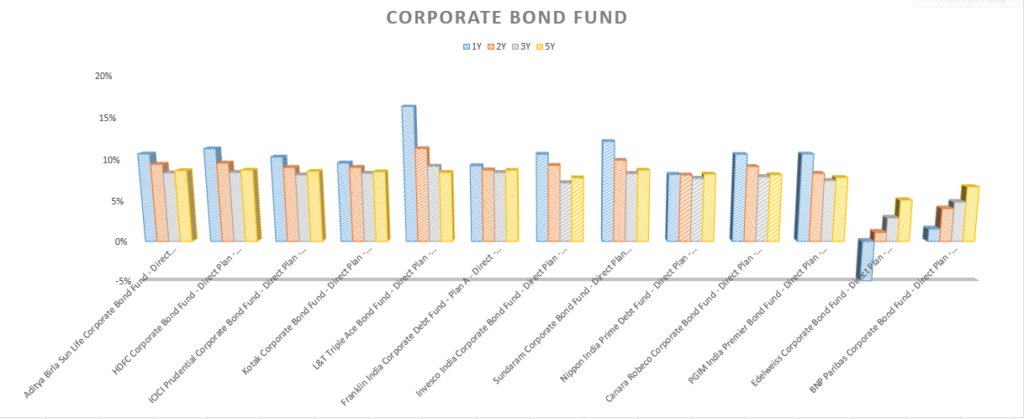

Corporate bond fund

Corporate Bond funds have a narrow mandate of investing mainly in the highest-rated corporate bonds.

Since these funds invest in a different category of companies there is a high chance of defaults if the AMC has invested in a company that doesn’t pay the money back. If you see the below chart; there are funds that have given negative returns in this category.

Performances of Corporate bond MFs over the last 5 years:

Should retail investors invest in Corporate bond funds?

- Yes – only if you can examine the investments of your fund

- No – If you don’t understand how the fund invests your money

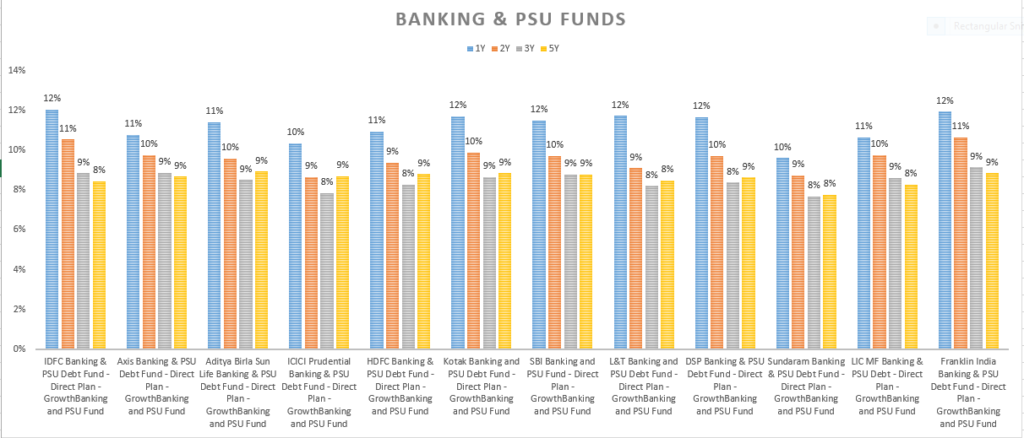

Banking and PSU funds

This is a fund that invests mainly in bonds issued by banks, public sector undertakings (PSUs), and public financial institutions.

Banking and PSU funds have done well in the last 5 years. There is no fund that has performed negatively.

Performances of Banking and PSU MFs over the last 5 years:

Should retail investors invest in Banking and PSU funds?

Yes-Since these funds invests in high-quality papers of banks and PSUs they are relatively safe. Remember that these funds do well when interest rates go down but they perform badly when interest rates go up.

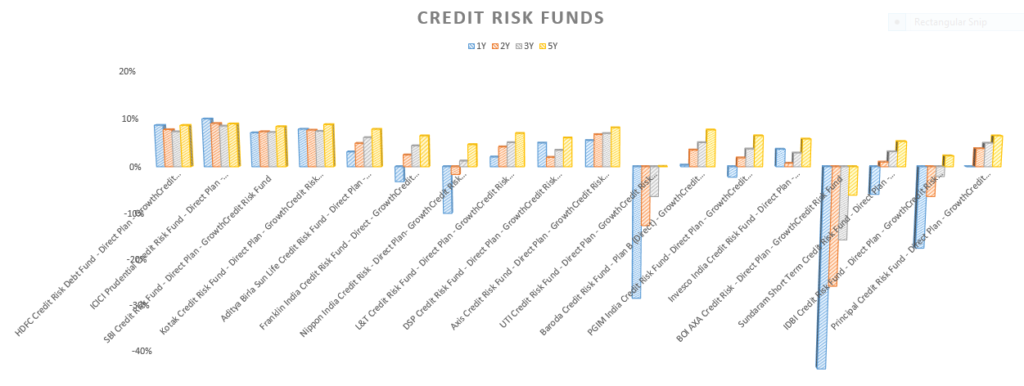

Credit risk funds

Credit risk funds invest mainly in corporate bonds which are below the highest rating assigned by credit rating agencies. The lower rating indicates a higher possibility of these bonds defaulting on repayment of investors’ money. Therefore, these funds are the riskiest of all types of debt funds.

However, they compensate for this additional risk with a higher return potential as these bonds offer better rates of interest than the highest-rated bonds. Moreover, investors can also benefit if the rating of these bonds is subsequently upgraded.

Performances of Credit risk MFs over the last 5 years:

Should retail investors invest in Credit risk funds?

No – This category is the most hit by the ongoing debt fund issues. Retail investors should avoid this fund category completely.

Are debt funds safe? – Conclusion

Earlier people used to ask are mutual funds safe. then they started asking are equity mutual funds safe? Now they are asking are debt mutual funds safe.

Are debt funds safe? – Yes they are safe if you understand the debt fund!

With the recent events, it’s clearly evident that the image of debt funds has taken a big dent. But at the same time, investors should understand that not all debt funds are bad. If you invest in good quality debt funds then you will be safe. Just make sure you understand the debt funds before you invest in it.

The Govt of India has started a debt fund ETF for its public sector companies called Bharat Bond ETF. It has 2 options Bharat Bond ETF 2023 and Bharat bind ETF 2030. These funds have papers of all public limited companies of rating AAA. This is an excellent option for retail investors to look at.

You can alternatively look at the Fund of Fund for Bharat bond ETF which is available as a mutual fund to invest in.

Do read – How to select mutual funds India?

Disclaimer – Mutual Fund investments are subject to market risks, read all scheme-related documents carefully.

Very useful article on all kinds of debt funds and their performance. But the labels are not clearly visible in the Bar graphs. IT would be great if you could pls. change them into a darker shade and bigger font.

Thanks